Best House Buying Companies in the UK 2026

Last updated: February 2026

The best house buying companies are genuine cash buyers that can prove funds, provide realistic pre-survey pricing, and complete in 7-28 days. In 2026, straight cash offers typically fall within 73-85% of market value, with standard legal fees usually covered.

Key takeaways:

- 73–85% of market value is the typical offer range from genuine cash buyers in 2026.

- Most reliable companies complete chain-free within 7–28 days.

- Proof of funds should be confirmed by your solicitor alongside TPO or NAPB membership.

This guide ranks the top 24 firms in 2026 so you can see who pays fairly and who can be trusted with backing from market data showing that in 2026, 32.8 % of UK homes sold via cash transactions. Let's see who made the cut.

-

- What are House Buying Companies

- Revealed: UK's Best House Buying Company

- How Much do they Pay for your Home in 2025?

- Is it Worth Selling to a House Buying Company?

- Regulations, Memberships & Code of Practice

- Types of Companies that Buy Houses

- Quick Sale Companies vs Estate Agents vs Auction

- How Companies that Buy your House Work

- Compare House Buying Companies

The Best Companies that Buy Houses in the UK are:

*Data verified: February 2026

Best for: Sellers who want maximum certainty with the UK’s only completion guarantee.

What they pay: Typically 75–85% of market value, depending on the property and timeline.

What we found: Housebuyers4u are genuine cash buyers using their own funds, providing proof via solicitors and offering transparent contracts with no option agreements. Offers are realistic, completions are achieved on time & legal fees are covered.

Accreditations: The Property Ombudsman, National Association of Property Buyers, National Association of Estate Agents & The Financial Conduct Authority.

Review Scores: 4.8/5 Trustpilot (1,247 reviews), 4.9/5 Google (892 reviews)

Media Coverage: Featured in Daily Mail, The Metro, Estate Agent Today

Unique Guarantee: The only company offering completion guarantee

Good fit if: You want a guaranteed sale inside 7-14 days, need to sell a property in poor condition, or simply value peace of mind above everything else.

Best for: Sellers looking for a quick initial offer.

What they pay: Typically 71–80% of market value.

What we found: HouseBuyFast are known for fast responses and clear communication. Initial offers are made quickly and solicitor coordination is generally smooth, although completion speeds depend on survey results.

Accreditations: Industry recognised; co-founder Jonathan Rolande is a well-known figure in the property sector.

Good fit if: You want a rapid start and straightforward paperwork, but don’t need a completion guarantee.

Read our entire HouseBuyFast review.

Best for: Sellers who want an ethical stance and steady service.

What they pay: around 70–82% of market value.

What we found: Open Property Group are members of both TPO and NAPB, and are regarded as ethical operators. Completion times are usually 7–14 days, and their process is transparent.

Accreditations: The Property Ombudsman; National Association of Property Buyers.

Good fit if: You want a reputable alternative with recognised memberships and clear timelines.

Best for: Sellers who want a straightforward cash sale with fees covered.

What they pay: Around 70–82% of market value.

What we found: Home House Buyers state they purchase using their own funds, offer chain-free sales, and cover legal fees. Completion is usually quoted between 7–28 days, depending on the property and checks.

Accreditations: The Property Ombudsman; National Association of Property Buyers.

Good fit if: You want a simple, no-chain sale and are flexible on price in exchange for speed.

Best for: Sellers who want clear pricing and a fast cash sale.

What they pay: Typically 70–85% of market value.

What we found: SmoothSale state they buy with their own funds, cover legal fees, and offer a guaranteed sale. Completion times are usually 7–14 days, subject to due diligence.

Accreditations: The Property Ombudsman; National Association of Property Buyers.

Good fit if: You want transparency on offer levels and a quicker sale without mortgage delays.

Want the full picture? See how all 23 companies stack up in our detailed comparison table

How We Ranked the Best House Buying Companies

We rank 24 UK house buying firms using five core signals, based on our team’s research into reputation, proven experience, seller feedback, funding sources, and industry accreditations.

- Proof of funds confirmed via solicitor

- Contract transparency (no option agreements)

- Speed and certainty to completion (days, fall-through risk)

- Independent review quality (Trustpilot, Google, Feefo)

- Industry accreditations (The Property Ombudsman, National Association of Property Buyers

What a Genuine Company That Buys Houses Looks Like in 2026

Based on our experience buying property and reviewing UK cash sale transactions, the following benchmarks are consistent across reputable house buying companies:

-

Typical first response time: 5–30 minutes

-

Realistic cash offer range: 73–85% of market value

-

Common red flag: Very high initial offers followed by delays or price changes

-

Strong trust signal: Proof of funds confirmed early via a solicitor

These benchmarks are used as a reference point when assessing each company in this guide. Firms that fall well outside these ranges tend to carry a higher risk of delays, renegotiations, or failed sales.

What are House Buying Companies?

House buying companies (also called cash house buyers) purchase properties directly from homeowners for cash, offering a fast, chain-free sale in exchange for a price below market value. They avoid estate agents, can complete in as little as 7-28 days, often cover legal fees, and buy properties in any condition. Sellers should always check whether the company is a genuine cash buyer or a broker, and verify proof of funds before proceeding.

How much do they pay for your Home in 2026?

Unfortunately, even with a traditional estate agent, you likely won't get full market value but for cash buyers.

In 2026 alone, 32.8% of home sales were to cash buyers, most citing ‘speed’ and ‘certainty’ as the top motivators for bypassing traditional estate agents.

How Have Offers from Cash House Buyers Changed? Our 5-Year Analysis

| Year | Average Price Offered |

|---|---|

| 2021 | 78–88% |

| 2022 | 75–87% |

| 2023 | 74–86% |

| 2024 | 74–85% |

| 2025 | 73–85% |

| 2026 | 73–86% |

We analysed market trends over the past 5 years and observed that the average percentage of market value offered by house-buying companies has remained steady, ranging from 73% to 85%. These figures are consistent across much of the UK property market, though London often sees stronger offers compared to the North of England.

In 2026 specifically, a home buying company's below market value offer will be approximately 73% to 86%.

Factors That Decrease Offers:

What Factors Affect How Much a House Buying Company Offers You?

This data chart further breaks down the crucial factors, explaining why the above factors carry the weight they do. Although quite a few will be out of your control, you can use these insights to make a difference in your property's valuation and sale price.

- Property location: Prime postcodes attract higher offers.

- Property condition: Better condition usually lifts the price.

- Required timeline: Urgent 7-day sales reduce the offer.

- Local demand: High demand can raise the range.

- Size and type: Larger or unique homes can command more.

- Legal or structural issues: Major issues reduce the offer.

- Economic climate: Weaker markets compress offers.

- Local trends: Micro-market strength matters.

Related Read: What is my house worth in 2026?

60-Second Trust Checklist (Before You Accept Any Offer)

1) Check trade body membership (30 seconds)

Search the company name on:

-

The Property Ombudsman

-

National Association of Property Buyers

If the company is listed then great, if not, proceed with caution.

2) Verify the company on Companies House (30 seconds)

Search the business on Companies House and confirm:

-

Status shows Active

-

Accounts are filed (not overdue)

-

Directors are clearly listed

Red flag: newly formed companies or multiple dissolved businesses linked to directors.

3) Confirm proof of funds (ask your solicitor)

Ask for written confirmation from the buyer’s solicitor showing:

-

Cash funds available now, or

-

An undrawn facility confirmed by a regulated lender

If they delay or avoid this, walk away.

4) Check the contract type (critical step)

Confirm the purchase is a straight sale, not:

-

An option agreement

-

A lock-in or exclusivity contract

-

Any restriction placed on your title

If you’re unsure, ask your solicitor to confirm in writing.

5) Agree the completion timeline in writing

Get written confirmation of:

-

Target completion date (for example, 7–28 days)

-

That the offer will not be reduced later unless new, material issues are found

No written confirmation = no deal.

National Association of Property Buyers

Property Ombudsman

Types of Companies that Buy Houses for Cash

Not all “cash buyers” are the same. When selling quickly, it’s crucial to know who you’re dealing with:

-

Genuine Cash Buyers: Have their own funds and can buy your home outright within weeks no loans, no waiting.

-

Non-Genuine Cash Buyers: May promise quick sales but often lack funds, undervalue properties, or depend on third parties.

-

Advisory/Middlemen Companies: Act as intermediaries, aiming to buy your home cheap and sell it on for a profit, often leaving you with less.

We conducted a report and here's how their offers typically compare on a £300,000 property:

| Service Provider | Service Fee | Typical Offer Range | Offer Amount (£300k House) |

|---|---|---|---|

| Traditional Cash Buyer | None | 70-80% of market value | £210,000 - £240,000 |

| iBuyer | 5-6% | 90-95% of market value | £270,000 - £285,000 |

| Cash Buyer Marketplace | £500-£1000 | Up to 100% of market value | Up to £300,000 |

| Home Trade-In Service | Varies | 85-95% of market value | £255,000 - £285,000 |

Quick Sale Companies vs Estate Agents vs Auction

| Feature | Company (Cash Buyer) | Estate Agent | Auction |

|---|---|---|---|

| Trustpilot Review Rating | 4.0 / 5 | 3.8 / 5 | 3.9 / 5 |

| Hidden Fees | Possible | Yes | Commission |

| Average Sale Time | 14–28 days | 4–6 months | 6–10 weeks |

| Guaranteed Sale (No Fall Through) | No | No | No |

| Agreed Sale Price | £235,000 | £265,000 | £222,400 |

| Fees (Estate Agent / Auction) | Varies | £8,340 | £6,672 |

| Conveyancing Fees | £1,500 | £1,500 | £1,500 |

| Sale Completion Certainty | ~90% | ~70% | ~90% |

| Viewings Required | None | Multiple | Scheduled |

| Total Received After Costs | £233,500 | £248,811 | £210,100 |

How Companies that Buy your House Work

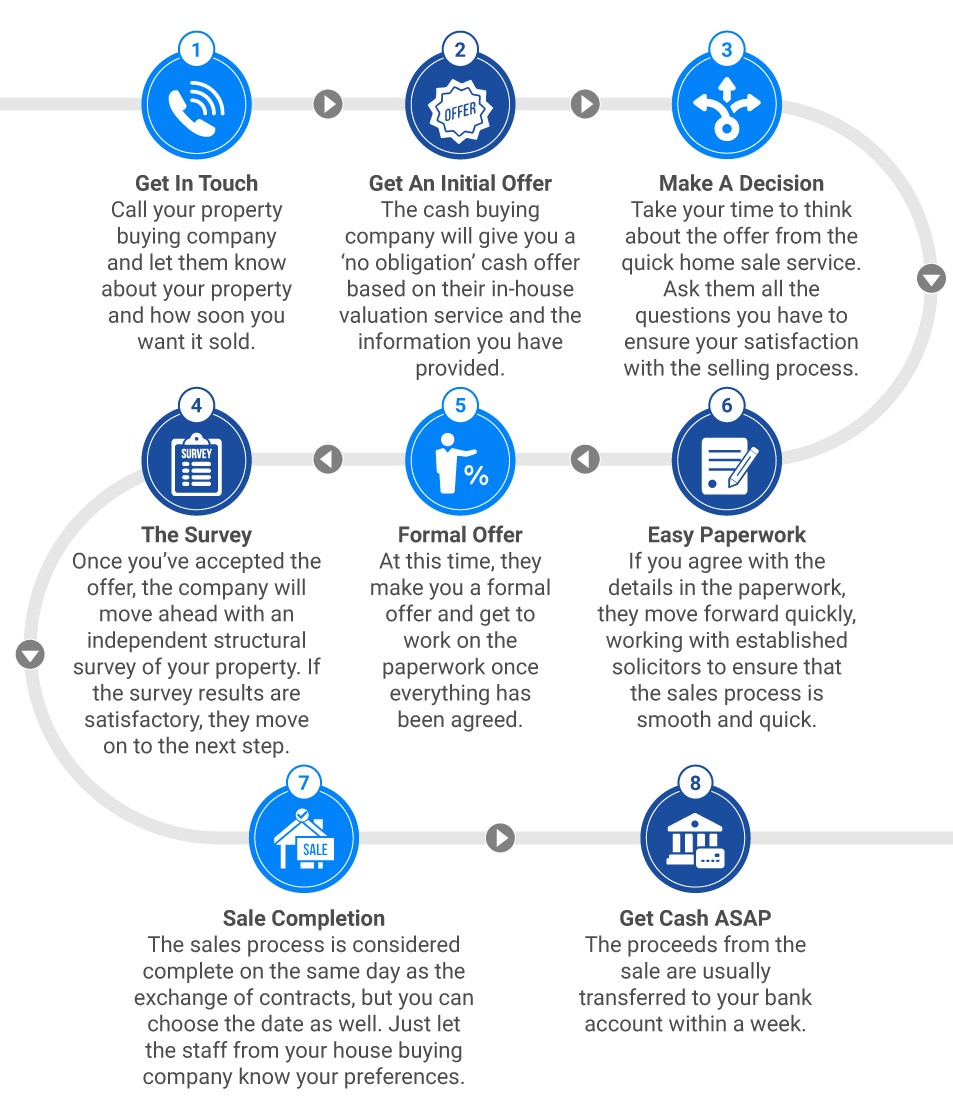

How the process works in 8 easy steps that guarantee completion.

Selling your home is a big decision, I understand that. You want it to go smoothly and feel worthwhile. Traditional selling can take months, involve lots of uncertainty, and fall through at the last minute. In contrast, reputable house buying companies offer a guaranteed sale, a fixed timeline, and a straightforward process that removes the usual stress and delays.

Additionally, going with a we buy houses service is straightforward. Here's how it goes:

1) Get In Touch: : Call the firm and tell them about your property and how soon you want to sell it.

2) Get An Initial Offer: Receive a no-obligation cash offer based on a quick in-house valuation.

3) Make A Decision: Review the offer and ask any questions before moving forward.

4) The Survey: The company arranges a structural survey to check for major issues such as damp issues.

5) Formal Offer: After the survey, you get a written offer and confirm if you want to proceed.

6) Easy Paperwork: Sign the paperwork; the company works with solicitors and covers legal fees.

7) Sale Completion: The sale completes on the agreed date, usually at the same time as the exchange.

8) Get Cash ASAP: The proceeds from the sale are usually transferred to your bank account within a week.

Timing from a recent Sale: (January 4th 2026)

- Initial contact to offer: Same day

- Decision period: 1–3 days

- Survey: 2–3 days

- Formal offer: 1 day

- Conveyancing: 7–14 days

- Funds landed: Same or next working day

That gives a total of roughly 11–23 days from first contact to cash received.

How Long Does Each Step Actually Take? (Housebuyers4u 2025-26 Data)

Most guides list the steps, but few show what actually happens in practice. Here’s our analysis and a report of our findings on what we’ve seen from hundreds of real Housebuyers4u customers this year:

| Step | Average Time Taken (2025-2026) | Customer Satisfaction (%) |

|---|---|---|

| Get In Touch | <1 day | 96% |

| Get An Initial Offer | 1 day | 93% |

| Make A Decision | 1-2 days | 90% |

| The Survey | 2-3 days | 89% |

| Formal Offer | 1 day | 91% |

| Easy Paperwork | 1-2 days | 92% |

| Sale Completion | 7-14 days | 89% |

| Get Cash ASAP | Same day/next day | 95% |

Expert advice from our property expert Paul

My advice to anyone in a similar position is to ask lots of questions don’t hesitate to make sure you fully understand the timeline and offer details before committing."

Compare House Buying Companies

The Best Quick House Sale Companies in the UK

Based on our January 2026 analysis, this table showcases the best companies that buy houses for cash in the UK. We’ve thoroughly reviewed each firm using the latest Trustpilot, Google, and Feefo ratings, so you can easily compare top cash buyers side by side. For full details, follow the links to our in-depth company reviews.

| House buying company | Trustpilot score | Google score | Feefo score |

|---|---|---|---|

| Housebuyers4u | 4.8 | 4.7 | 4.7 |

| HouseBuyFast | 4.0 | 4.7 | 4.8 |

| Quickmovenow | 4.3 | 4.4 | 4.9 |

| Goodmove | 4.9 | 4.8 | No reviews |

| Property Solvers | 4.7 | 4.8 | No reviews |

| National Homebuyers | 4.5 | 4.1 | No reviews |

| Open Property Group | 4.7 | 4.3 | 4.9 |

| British Home Buyers | 4.9 | 4.9 | No reviews |

| Ready Steady Sell | 3.7 | No reviews | No reviews |

| We Buy Now | 4.4 | 4.1 | No reviews |

| SpringMove | 4.5 | No reviews | No reviews |

| TheAdvisory | No reviews | 5.0 | No reviews |

| Ask Susan | No reviews | 2.3 | No reviews |

| Property Cash Buyers | 1.3 | No reviews | No reviews |

| We Buy any Home | 4.0 | 3.9 | No reviews |

| Home House Buyers | 4.9 | 4.9 | No reviews |

| Smooth Sale | 4.9 | 4.9 | No reviews |

| Upstix | 4.0 | 4.2 | No reviews |

| Express Offers | 4.1 | No reviews | No reviews |

| Sold | 4.5 | 3.5 | No reviews |

| House Buyer Bureau | 4.5 | 4.6 | No reviews |

| Zoom Property Buyer | 4.6 | 3.0 | No reviews |

| Bettermove | 4.6 | No reviews | No reviews |

| Sell House Fast | 4.7 | No reviews | No reviews |

*Note: Review data is usually less than 12 months old, please click and read the individual reviews above for up to date details on each website.