How it works

Services

Sell your House Fast

How Much is Your House Worth

Selling Guides

Companies that Buy Houses

Best Time to Sell your House

How Long It Takes to Sell a House

Selling Situations

Broken House Chain (Fallen through)

Relocating or Emigrating Sale

Financial Difficulties (Release Cash)

Sell House After Divorce

Selling Inherited Property (UK)

Selling a Tenanted property

Selling a Probate Property

Sell a House in Any Condition

Stop House Repossession

Sell your Flat Quickly

Company Reputation Check (Guide)

Conveyancing Guide

Blog

About us

About our Company

Reviews

Success stories

Press & Media

FAQ

Contact us

Free Cash Offer

✕

Filter by

Categories

Tags

Authors

Show all

All

Auctioning your house

Buying a house

Debt help

Estate agents

House selling advice

Landlords

Miscellaneous

Property market news

Quick sale house buyers

Saving money

Success stories

Tenants & Renting

Tools and Calculators

All

add value

add value home

annuity

apartment

ar

arrears

article

auction house

auctions

augmented reality

avard

avoid

avoid repossession

bad credit

bad shape

bargain

best day to sell

best month to sell

best time to sell

bridgfords

broken chain

bungalow

buy

buy house auction

buy your house

buyer

buying

capital gains

care

carer

cash buyers

cash house buyer

certificate

chain free

charters

checklist

cleaning

contracts

conveyancer

cottage

credit

credit report

credit score

damp

damp issues

debt

debt help

detached

devalue

disrepair

divorce

divorced

diy

diy house sale

downsizing

emigrating

emigration

end of terrace

energy

energy label

energy performance certificate

epc

equity

estate agent

financial difficulties

financial diffuculties

financial problems

fine and country

first time home buyer

first time homebuyers

flat

flats

foundation

foxtons

fraud

freehold

garden

gas

haggle

health problems

home

home buyer

home chain

home repossession

home security

home staging

house

house buyers

house buyers survey

house chain

house not selling

house repossession

house selling process

housebuyers

housing chain

how long to sell a house uk

how long to sell house

how to sell a house

ill health

illness

inherited property

jan forster

japanese knotweed

jeffery ross

JLL

job loss

kerb appeal

landlord

leasehold

market value

mistakes

mortgage

mortgage arrears

mortgages

moving abroad

negative equity

negotiate

neighbor

neighborhood

new build

news

offer

overseas

pension

pets

planning permission

poor condition

poor health

private house sale

problem properties

problem property

property

property agent

property chain

property deeds

property fraud

property type

quick sale company

quick sale firm

quick sale house buyers

quick sale property

real estate

reduce debt

redundancy

relocating

relocation

renovation

rent

rent house

rent landlord

rent property

renting

repossessed

repossession

repossession process

retire

retirement

reviews

run down

scams

seasons

security

seddons

sell home

sell house

sell house auction

sell house no agent

sell house uk

sell my house

sell online

sell property

selling house auction

semi-detached

shared equity

shared ownership

solar energy

solar panels

solicitor

squatters

stop repossession

stress

structural damage

structural problems

supply and demand

surveyor

tax

tenant

terraced

to let

traffic

turn offs

utility bills

virtual reality

virtual tours

vr

we buy any house

we buy any house review

worst time to sell

All

Harry

housebuyers4u

Pamela Policarpio

June 16, 2025

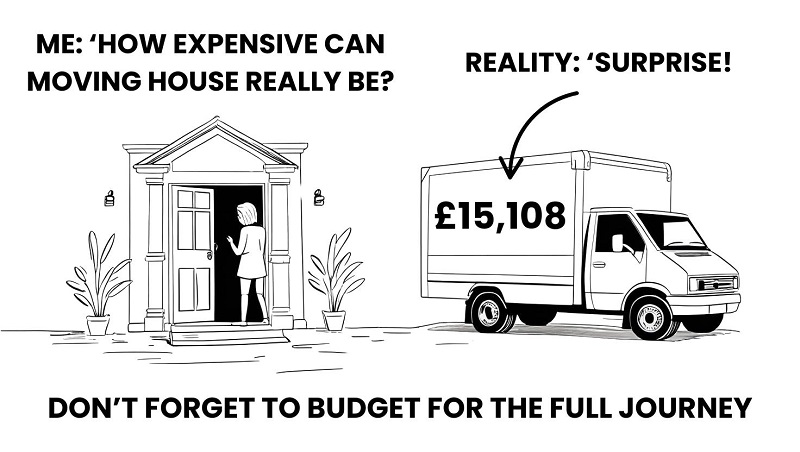

How Much Does It Cost to Move House in 2025?

May 21, 2025

What is Gazumping and Why Do Buyers Dread It?

May 13, 2025

Should I Sell My House to Pay Off Debt? (Pros & Cons)

April 30, 2025

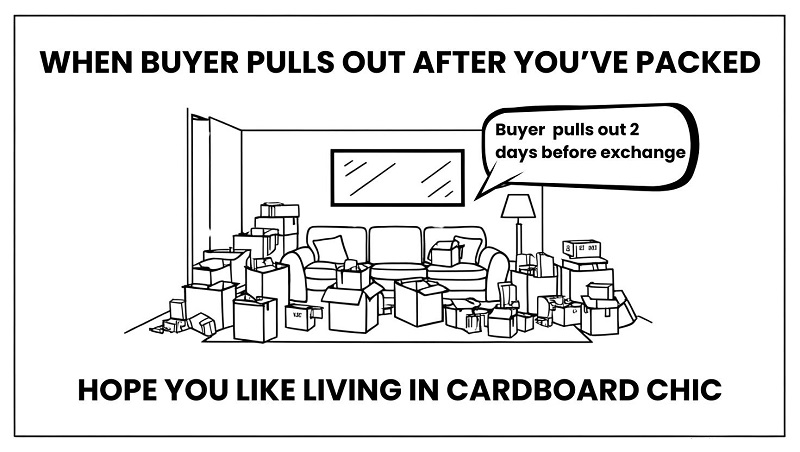

Pulling Out of a House Sale: Legal Rules, Costs & What Happens Next

April 29, 2025

What is Gazundering? (How to Avoid & Respond If It Happens)

April 23, 2025

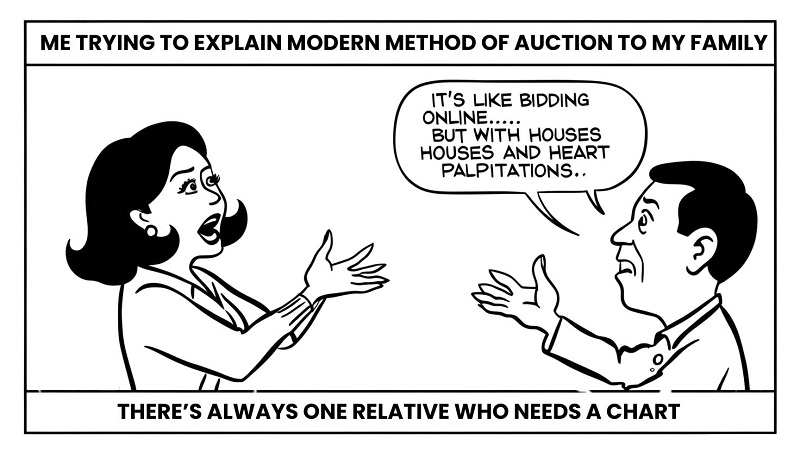

Modern Method of Auction Explained (+ Pros & Cons)

April 22, 2025

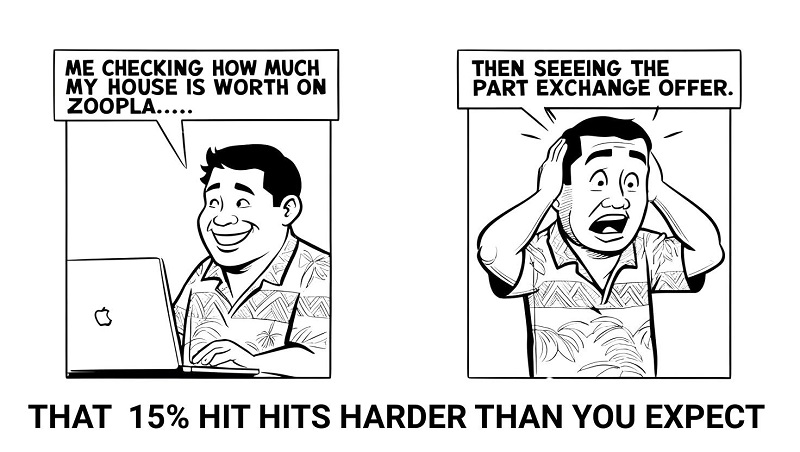

Part Exchange House Explained (Is it Worth it in 2025?)

April 21, 2025

Sold STC (Subject to Contract): What Does it Mean?

April 16, 2025

Renting in Retirement: 7 Things to Consider Before You Decide (2025)

Load more