Pulling Out of a House Sale: Legal Rules, Costs & What Happens Next

Updated: March 2026

A buyer pulls out just days before completion, and suddenly your whole move is at risk. It’s more common than you think. In the UK, you can legally pull out of a house sale at any point before the exchange of contracts. While it’s legal, it can still cost you thousands and significantly delay your plans.

Key Takeaways:

- You can pull out before exchange with no legal penalty, but you may lose £1,000-£3,000+ in costs.

- After the exchange, pulling out can lead to losing your deposit or being sued for breach of contract.

- Most failed sales happen before exchange, often due to surveys, mortgage issues, or chain collapse.

-

- Can You Legally Pull Out of a House Sale in the UK?

- What Happens If the Seller Pulls Out? (If You're the Buyer)

- Can You Pull Out of a Sale If You're the Seller?

- Common Reasons for Pulling Out of a House Sale

- What It Might Cost to Pull Out

- Need Certainty? Consider a Guaranteed Buyer

- Frequently Asked Questions

Can you pull out of a house sale in the UK?

Yes. In England and Wales, buyers and sellers can withdraw from a house sale at any point before contracts are exchanged because the agreement is not legally binding. After the exchange, the sale becomes legally enforceable, and pulling out can result in financial penalties, loss of deposit, or legal action.

When Can You Pull Out of a House Sale?

| Stage | Can you pull out? | Legal risk | Financial impact |

|---|---|---|---|

| Before exchange | Yes | None | Loss of fees |

| After exchange | No | Breach of contract | Deposit loss + legal costs |

What Does “Subject to Contract” Mean?

“Subject to contract” means a property deal is not legally binding, even if both the buyer and seller have agreed on a price.

In England and Wales, nearly all house sales are agreed on this basis. It allows either party to pull out at any point before contracts are exchanged without legal consequences.

This is why sales can fall through late in the process. Until contracts are formally signed and exchanged, nothing is guaranteed.

Read our full guide on everything you need to know about sold STC

What Happens If the Seller Pulls Out? (If You're the Buyer)

If the seller pulls out of a house sale before contracts are exchanged, there's usually little you can do to stop it. The agreement isn't legally binding until exchange, so the seller can change their mind, accept another offer, or take the property off the market altogether.

According to Mortgage Solutions, 37% of buyers were gazumped in 2024, with the average out-of-pocket loss sitting at £2,400. This is why it's important to be aware as a buyer otherwise you could lose out on thousands.

Is It Legal for the Seller to Pull Out?

Yes. In England and Wales, the seller is legally allowed to pull out at any time before exchange of contracts. They don’t need a specific reason and aren’t obliged to reimburse any costs you’ve incurred.

In Scotland, sellers can only pull out before the conclusion of missives. After that point, they’re legally committed to the sale.

What Costs Will You Still Owe?

Even if the seller pulls out, you're still responsible for any expenses you’ve already committed to. These might include:

| Cost Type | Typical Amount | Refundable |

|---|---|---|

| Survey or valuation fees | £250–£800+ | No |

| Mortgage application fees | £200–£500 | No |

| Conveyancing/legal work | £500–£1,000 (depending on stage) | No |

| Local authority searches | £150–£400 | No |

Can You Sue the Seller?

If the seller pulls out before exchange, the answer is almost always no. There’s no legal contract, so they’re within their rights to walk away.

If they pull out after exchange, you may be able to:

-

Reclaim your deposit

-

Claim compensation for financial losses

-

Take legal action for breach of contract

Legal action is rare but possible, especially if you’ve lost money due to the collapse of a confirmed sale.

Is There Anything You Can Do?

In some cases, yes. If you really want the property and the seller is open to discussion, you could:

-

Increase your offer (if you’ve been gazumped)

-

Offer to delay the sale if the seller’s circumstances have changed

-

Suggest pausing the process rather than ending it

This won’t always work — but for sellers facing temporary issues or chain problems, flexibility might keep the deal alive.

If the seller won’t budge, your best move is to restart your search quickly and avoid further delays. You may also want to consider getting Home Buyer Protection Insurance for your next attempt.

Can You Pull Out of a Sale If You're the Seller?

Yes — as the seller, you can pull out of a house sale at any point before contracts are exchanged. There’s no legal penalty for doing so, though it can still come with practical and financial consequences.

Pulling Out Before Exchange

Until contracts are exchanged, the sale isn’t legally binding. You’re free to withdraw your property from the market, accept a higher offer, or change your mind entirely.

However, you may still face:

-

Wasted time for everyone involved

-

Frustration or reputational damage with agents or buyers

-

Loss of any fees you’ve already paid (e.g. solicitor or admin costs)

If you're using an estate agent, check your agreement. Some agents include clauses that require payment if they’ve introduced a “ready, willing and able” buyer — even if you pull out.

Pulling Out After Exchange

Once contracts are exchanged, you're legally committed to the sale. Pulling out at this stage is a breach of contract and could lead to:

-

A notice to complete from the buyer (giving you 10 days to finalise the sale)

-

Daily interest penalties

-

A potential lawsuit for damages

-

Having to refund the buyer’s deposit and cover their legal costs

In most cases, it’s cheaper and safer to complete the sale than face a legal battle.

Expert advice from our property expert Paul Gibbens:

"We’ve seen plenty of sellers panic about pulling out of a sale, especially when things change last-minute. If it’s before exchange, you’re legally in the clear — but it’s still important to think about the practical fallout. You might lose money on legal work, frustrate the chain, or damage your chances of a smooth future sale.

After exchange, the risks are much higher, and in most cases, it makes more sense to push through than face legal claims or compensation payouts."

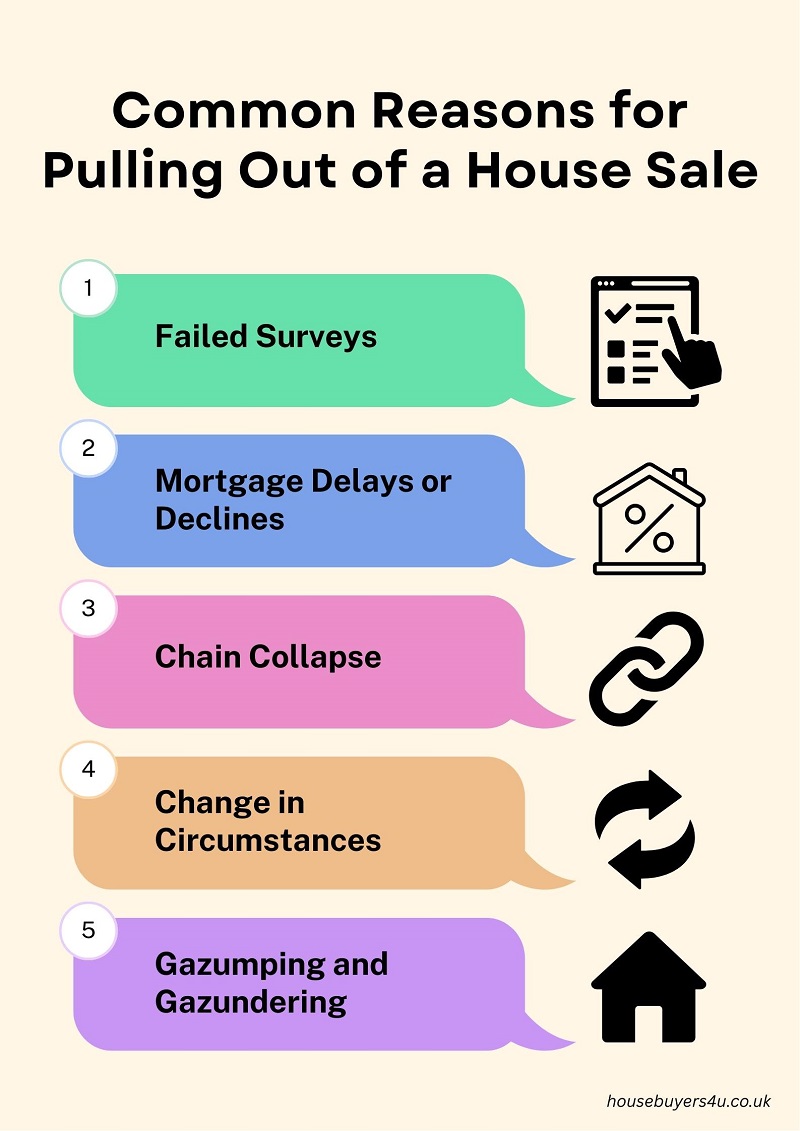

Common Reasons for Pulling Out of a House Sale

Pulling out of a house sale can be frustrating — but it's more common than most people realise. Buyers and sellers back out for all sorts of reasons, and many are beyond their control.

1) Failed Surveys

One of the most frequent reasons buyers pull out is a poor survey result. Issues like damp problems, subsidence, roof damage or asbestos can quickly raise red flags. If the cost of repairs is too high, many buyers choose to walk away rather than renegotiate.

2) Mortgage Delays or Declines

A buyer might have a mortgage in principle, but that doesn’t guarantee approval. If their lender down-values the property or rejects the full application, they may be forced to pull out — even after making an offer.

Related Read: What is a down valuation?

3) Chain Collapse

Sales often fall through because of issues elsewhere in the property chain. If another buyer or seller in the chain backs out, the entire process can grind to a halt. This is a common reason sellers or buyers are forced to withdraw, even when they still want to go ahead.

4) Change in Circumstances

Job changes, family issues, bereavement, or financial setbacks can all affect someone’s ability to buy or sell. A seller might no longer need to move, or a buyer may no longer be in a position to proceed.

5) Gazumping and Gazundering

-

Gazumping happens when a seller accepts a higher offer after already agreeing to sell.

-

Gazundering is when a buyer lowers their offer at the last minute, hoping the seller is too far into the process to say no.

Both are legal in England and Wales, though often seen as unfair. They regularly lead to one party pulling out.

According to TheNegotiator in 2024, failed surveys were the leading cause of house sales falling through, accounting for 27% of collapsed deals. Buyers often demanded significant discounts after discovering issues like damp, subsidence, or structural problems, leading many sellers to withdraw rather than renegotiate

What Should You Do If a Sale Falls Through?

If your house sale falls through, the key is to act quickly and avoid losing further time or money. What you do next can make a big difference to how smoothly you recover.

-

Act quickly to re-list or restart your search

The longer you wait, the more likely you are to lose momentum or miss out on other opportunities. Sellers should get the property back on the market fast, while buyers should resume their search straight away. -

Review what caused the collapse

Identify the root issue. Was it a failed survey, mortgage problem, or chain breakdown? Understanding this helps you avoid the same problem happening again. -

Consider breaking the chain

Chains are one of the biggest reasons sales fall through. If possible, look at options that reduce reliance on other transactions, such as selling first or using chain-free buyers. -

Reassess your timelines and finances

A failed sale can impact your moving plans, mortgage offers, or onward purchase. Take a step back and make sure your timeline still works financially and practically. -

Consider alternative selling routes

If you’ve had multiple fall-throughs or need certainty, it may be worth exploring other options. Chain-free or cash buyers can remove many of the risks that come with traditional sales.

In most cases, the quicker you regroup and adjust your approach, the better your chances of securing a successful sale next time.

What It Might Cost to Pull Out (or Lose a Sale)

Even if you're legally allowed to pull out of a house sale before exchange, that doesn’t mean it’s free. Both buyers and sellers can lose money when a deal falls through — and in some cases, it can run into the thousands.

Typical Costs for Buyers

If the seller pulls out before contracts are exchanged, buyers often still have to pay for:

-

Surveys and valuations (£250–£800+)

-

Mortgage application or adviser fees (£200–£500)

-

Conveyancing work already carried out by a solicitor (£500–£1,000)

-

Local authority searches (£150–£400)

These costs are rarely refundable, unless the buyer has Home Buyer Protection Insurance.

Typical Costs for Sellers

While sellers don’t usually pay legal penalties for pulling out before exchange, they may still face:

-

Estate agent fees, depending on the contract (especially if they found a willing buyer)

-

Solicitor fees for work already done

-

Wasted time that can delay future plans or chain progression

If they pull out after exchange, they may also have to:

-

Return the buyer’s deposit

-

Cover legal costs

-

Pay interest or compensation if served with a notice to complete

When Is a Deposit Lost?

-

If the buyer pulls out after exchange, the seller typically keeps the 10% deposit.

-

If the seller pulls out after exchange, the buyer can usually claim the deposit back — and may also sue for damages.

Related Read: How much deposit do i need to put down for a house?

Need Certainty? Consider a Guaranteed Buyer

If you’ve just lost a buyer or are fed up with deals falling through, there is another option.

At Housebuyers4u, we work with pre-approved cash buyers who can complete in as little as 7–14 days. There are no estate agent fees, no delays, and no last-minute surprises.

Whether you're selling due to a chain collapse, financial pressure, or just want a quick, stress-free move — we’re here to help.

Get your free, no-obligation cash offer today.

Find out how much we can Offer for your House