What is Negative Equity & How to Get Out of It?

Updated: December 2025

If your mortgage is bigger than what your home is worth, you’re not alone. Thousands of UK homeowners find themselves in negative equity, especially after dips in the housing market. It can be worrying, but there are practical steps you can take to manage it and move forward.

3 Key Takeaways:

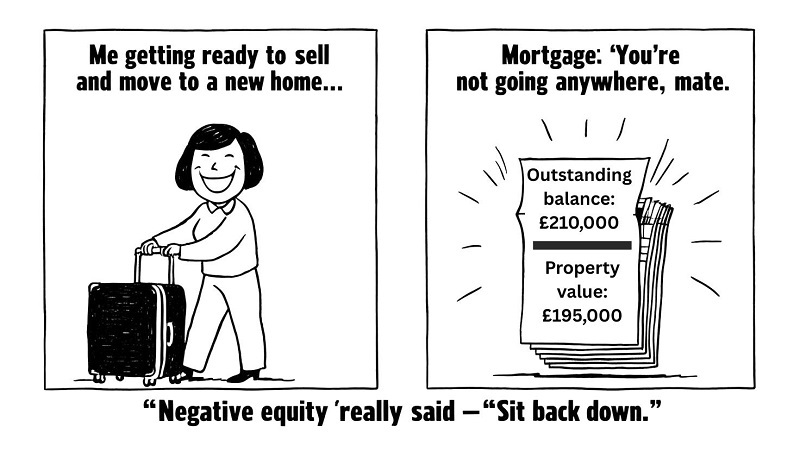

- Negative equity means your mortgage is higher than your home’s current value.

- It affects your ability to move, remortgage, or secure better interest rates..

- You can tackle it by overpaying, waiting for prices to rise, or renegotiating your mortgage.

How to Check if You’re in Negative Equity

To find out if you’re in negative equity, just follow these simple steps:

| Step | What to Do |

|---|---|

| 1. Check Mortgage Balance | Look at your latest mortgage statement or contact your lender. |

| 2. Get a Property Valuation | Use a local estate agent or an online valuation tool to estimate your home's value. |

| 3. Do the Calculation | If your home’s value is less than your mortgage balance, you’re in negative equity. |

Related Read: How much is your house worth?

How to Get Out of Negative Equity

If you’re stuck in negative equity, there are practical steps you can take to reduce or eliminate it over time:

-

Overpay your mortgage: Making extra payments reduces the amount you owe and helps rebuild equity faster. Always check for overpayment limits to avoid early repayment charges.

-

Wait for house prices to recover: If you're not planning to move soon, holding on until the market improves may naturally lift you out of negative equity.

-

Consider a negative equity mortgage: In rare cases, some lenders offer mortgages that let you transfer negative equity to a new property. These usually come with higher rates and conditions.

-

Rent out your property: If your lender agrees, renting your home could help cover repayments while you wait for prices to recover. You may need to pay a ‘consent to let’ fee and switch to a buy-to-let mortgage.

As of November 2024, the average UK house price rose to £290,000 - a £10,000 increase in just 12 months.

If this trend continues, homeowners in negative equity may see their equity position improve without taking further action, simply by holding on until the market recovers.

Expert advice from our property expert Paul Gibbens:

"In many of the cases I’ve dealt with, the best first step out of negative equity is overpayment; even small monthly contributions can make a big difference over time. But it’s not one-size-fits-all. If someone is unable to wait or needs to relocate quickly, we have also helped them explore options such as renting out the property or negotiating directly with lenders.

The key is not to pani,c there are always routes forward."

How to Avoid Negative Equity in the Future

While you can’t control the housing market, there are smart steps you can take to reduce your risk of falling into negative equity:

-

Put down a larger house deposit: The more you put in upfront, the more equity you start with, providing a buffer if prices fall.

-

Choose a repayment mortgage: Unlike interest-only deals, repayment mortgages reduce your debt over time, steadily building your equity.

-

Buy at the right time: Avoid buying when property prices are inflated. Research market trends and consider consulting with a local agent before making a commitment.

Negative Equity vs Negative Debt-to-Equity Ratio

In property terms, a negative debt to equity ratio simply means your mortgage debt is higher than the current market value of your home, in other words, you’re in negative equity. While the phrase is more commonly used in business or finance, it describes the same situation: your asset (the property) is worth less than the debt secured against it. In residential property, this often happens when house prices fall or a large deposit wasn’t put down at the start.