How to Avoid a Down Valuation?

Updated: December 2025

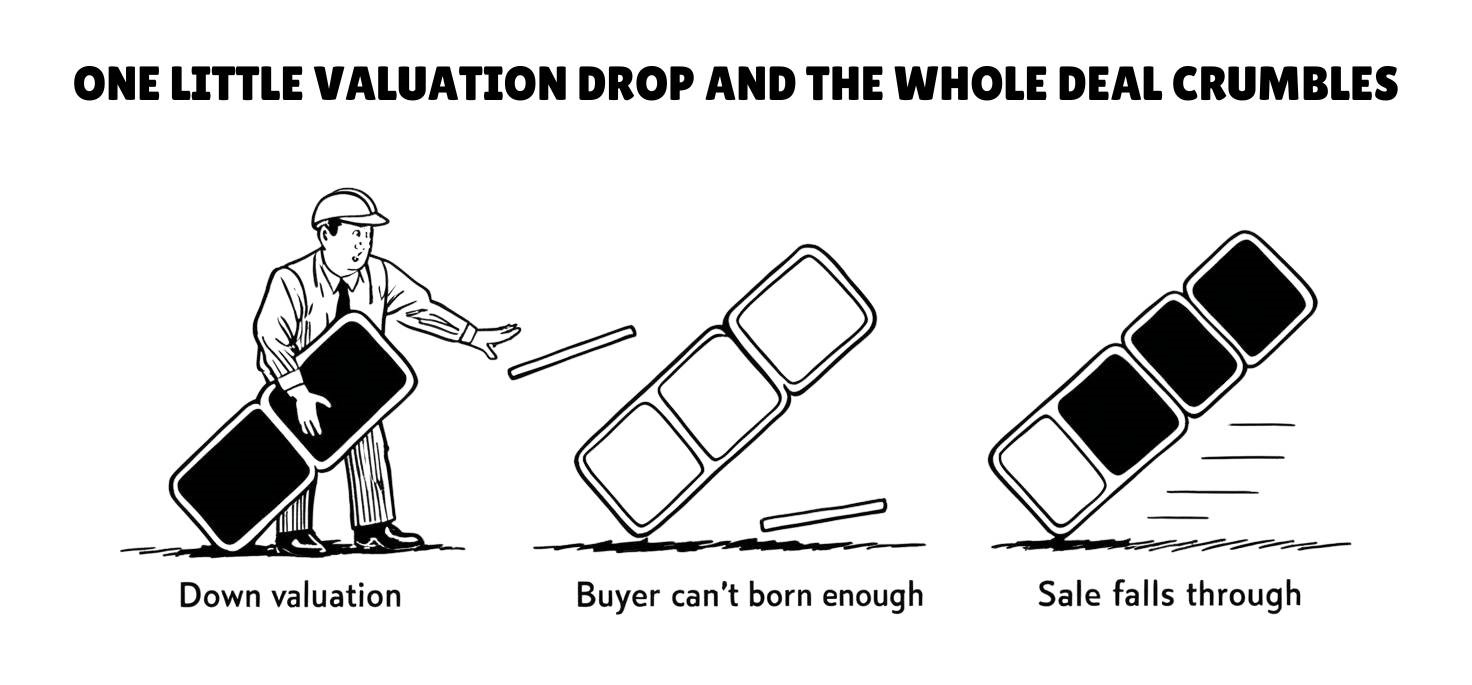

A down valuation occurs when a lender’s surveyor values a property lower than the agreed sale price, reducing the buyer’s borrowing power. This can lead to delays, price renegotiations, or even failed sales. For sellers, a down valuation can be frustrating, but there are ways to prevent or handle it. Pricing realistically, backing up your valuation with strong evidence, and preparing for the survey process can help ensure a smooth transaction.

Key Takeaways:

- A down valuation happens when a lender’s surveyor values a property below the agreed sale price.

- This can delay sales as buyers may struggle to secure their mortgage.

- Sellers can avoid this by pricing correctly, providing evidence, and addressing issues early.

What is a Down Valuation?

A down valuation is when a mortgage lender’s surveyor values a property lower than the price agreed between the buyer and seller. This means the lender will only base the mortgage on the lower figure, creating a shortfall the buyer must cover or prompting both parties to renegotiate. Down valuations commonly occur when offers are pushed up by market competition or optimistic pricing, and the lender needs to ensure the property genuinely supports the loan amount.

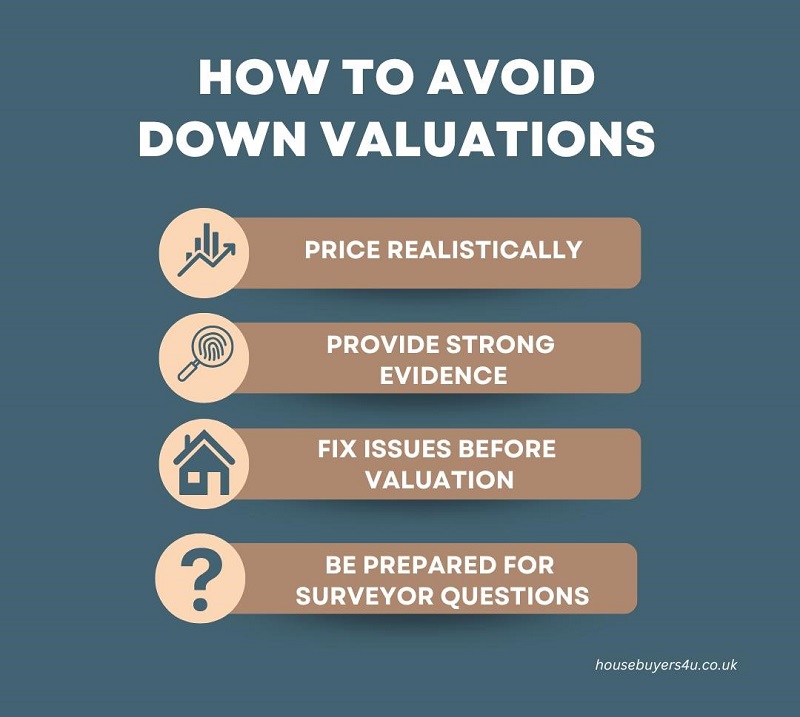

How to Avoid Down Valuations

Down valuations can delay or derail a sale, but taking the right steps early can help prevent them.

Price Realistically: Overpricing is a major cause of down valuations. Base your price on recent sold prices, not just estate agent estimates. Getting an independent RICS valuation can provide an accurate market value, and remember that renovations don’t always add as much value as expected.

Provide Strong Evidence: Lenders trust hard data, so have recent comparable sales figures, planning permissions, and renovation records ready. For new builds or major upgrades, showcase warranties and receipts to justify the price.

Fix Issues Before Valuation: Surveyors look for problems like damp, leaks, structural cracks, and outdated wiring, which can lower a property’s value. Address these issues beforehand to avoid a negative assessment. Even minor repairs can help maintain your asking price.

Be Prepared for Surveyor Questions: Surveyors rely on data but will also factor in seller-provided information. Ensure all renovations have the correct approvals, be ready to answer questions about disputes or past maintenance, and have documents like EPCs, damp-proof warranties, and structural reports available. A well-documented home reassures surveyors and supports your valuation.

Advice from our Property Expert Paul:

"Our conveyancing team has handled countless cases where sellers faced unexpected down valuations. They have told me personally and I also recommend that the best way to avoid this is to price realistically, back it up with strong evidence, and ensure your property is in good shape before the surveyor arrives.

Sellers who prepare properly are far less likely to see their sale fall through!"

Related Read: What do surveyors look for when valuing properties

Why Do Down Valuations Happen?

| Reason | Explanation |

|---|---|

| Overpricing | If the asking price is too high compared to recent sales, lenders may down value the property. They base valuations on actual sold prices, not current listings. |

| Market Conditions | In uncertain markets or during price drops, lenders take a cautious approach to avoid financial risk, leading to more conservative valuations. |

| Surveyor Valuation Methods | Surveyors use local comparable sales, but if they reference lower-value properties or lack area knowledge, it can result in an inaccurate valuation. |

| Property Issues | Structural defects, damp, outdated wiring, or invasive plants like Japanese knotweed can lead to a lower valuation, as lenders factor in repair costs. |

| Unproven Improvements | Renovations or extensions without proper approvals or documentation may not add as much value as expected, reducing the surveyor’s valuation. |

Sellers can reduce the risk of a down valuation by pricing correctly, addressing property concerns, and providing strong supporting evidence to justify their asking price.

Recent research from Zoopla suggests that nearly half of UK properties have been down valued in recent years, with homes between £400,000 and £500,000 most affected. If you’re selling in this price range, expect lenders to be more cautious and prepare strong valuation evidence to support your asking price.

One of the biggest frustrations for sellers is seeing a sale fall through due to a down valuation, but those who take the right steps can avoid this issue. Here’s what one of our sellers had to say:

Using Housebuyers4u, the whole process went smoothly from start to finish.Jackie was extremely patient, kept me informed at every stage answered any concerns I had, excellent customer service.

The solicitors, William's and co were equally approachable every step of the way. USE them, if you need to sell quickly.

What to Do If Your Property Gets Down Valued

A down valuation doesn’t have to mean the end of your sale. Sellers have several options to keep the transaction on track and work around the lower valuation.

Negotiate with the Buyer: If the buyer’s mortgage offer is reduced, they may ask for a lower price to match what their lender is willing to finance. Being flexible and open to negotiations can help avoid delays or a collapsed sale. Some buyers may agree to split the difference or cover the shortfall themselves if they’re keen on the property.

Challenge the Valuation: If you believe the surveyor’s assessment is unfair, gather evidence of comparable recent sales and request a reconsideration. A strong case can sometimes lead to the lender revising their decision. Your estate agent may also assist by providing valuation data from similar properties in the area.

Find a New Buyer or Lender: If negotiations fail, a different lender or a cash buyer may be an option. Mortgage providers don’t always use the same surveyors, meaning another lender could assess the property at a higher value. If time allows, consider relisting the property to find a buyer with more flexible financing.

Fix Issues That Caused the Down Valuation: If the valuation flagged concerns such as damp, roofing problems, or outdated wiring, addressing these before relisting the property can help justify your asking price. Even small improvements can make a difference and give future buyers more confidence in the property’s value.

Related Read: How much is my house really worth?

How Often Do Down Valuations Happen? (2024–2025 HB4U Data)

At Housebuyers4u, we track down valuations across the UK through sellers who come to us after a sale falls through. Our 2024–2025 internal data shows that down valuations are still common, especially in higher-value or cooling markets. Here is a snapshot of what we saw over the last 18 months.

| Price Range | % of Sales Affected (2024–25) | Most Common Reason |

|---|---|---|

| £200,000–£300,000 | 22% | Overpricing compared to recent sold prices |

| £300,000–£400,000 | 31% | Lender caution and weaker comparables |

| £400,000–£500,000 | 43% | Surveyors referencing lower-value comparables in slower markets |

Struggling with a Down Valuation? Find Out How We Can Help

A down valuation can be frustrating, but it doesn’t have to derail your plans. Whether your buyer’s mortgage offer has been reduced or your property has been undervalued, you still have options.

At Housebuyers4u, we buy houses directly for cash, meaning no surveys, no mortgage lenders, and no risk of down valuations. If you're struggling to sell due to a low valuation, we can give you a guaranteed sale with zero hassle—no waiting, no renegotiations, just a straightforward offer.

Don’t let a down valuation hold you back. Get a free, no-obligation cash offer today and sell your home stress-free!