Indemnity Insurance for Property Sellers: Essential Guide for a Smooth Sale

Updated: July 2025

Indemnity insurance is a one-time policy that protects property buyers and, in some cases, sellers from legal risks such as missing documents, planning issues, or outdated restrictions. If your house sale encounters a legal snag, this insurance is typically the quickest way to keep things moving and avoid delays or a collapsed chain.

- Indemnity insurance fixes legal problems that could block your house sale.

- It’s necessary when a solicitor identifies an issue that might deter buyers or lenders.

- The policy is usually arranged by your solicitor and paid for by the seller.

-

- What is Indemnity Insurance When Buying a House

- When and Why You Need an Indemnity Insurance

- Indemnity Insurance Cost: What You Need to Know

- How to Obtain an Indemnity Insurance

- Legal Framework of Indemnity Insurance

- Mortgage-Related Indemnity Insurance

- Final Thoughts & Key Takeaways

- FAQs on Indemnity Insurance

When Is Indemnity Insurance Needed in a House Sale?

Indemnity insurance is necessary in a house sale when a legal issue, such as missing FENSA certificates, unauthorised building work, old restrictive covenants, or missing planning paperwork, comes to light during the conveyancing process and could delay or block the sale. If problems like these aren’t resolved, buyers or their mortgage lenders may pull out, so getting indemnity insurance quickly is often the fastest way to keep your sale on track and avoid a collapsed chain.

According to the UK government, more than 300,000 property transactions fall through every year, costing sellers roughly £400 million annually, with many failures linked to legal or conveyancing hiccups.

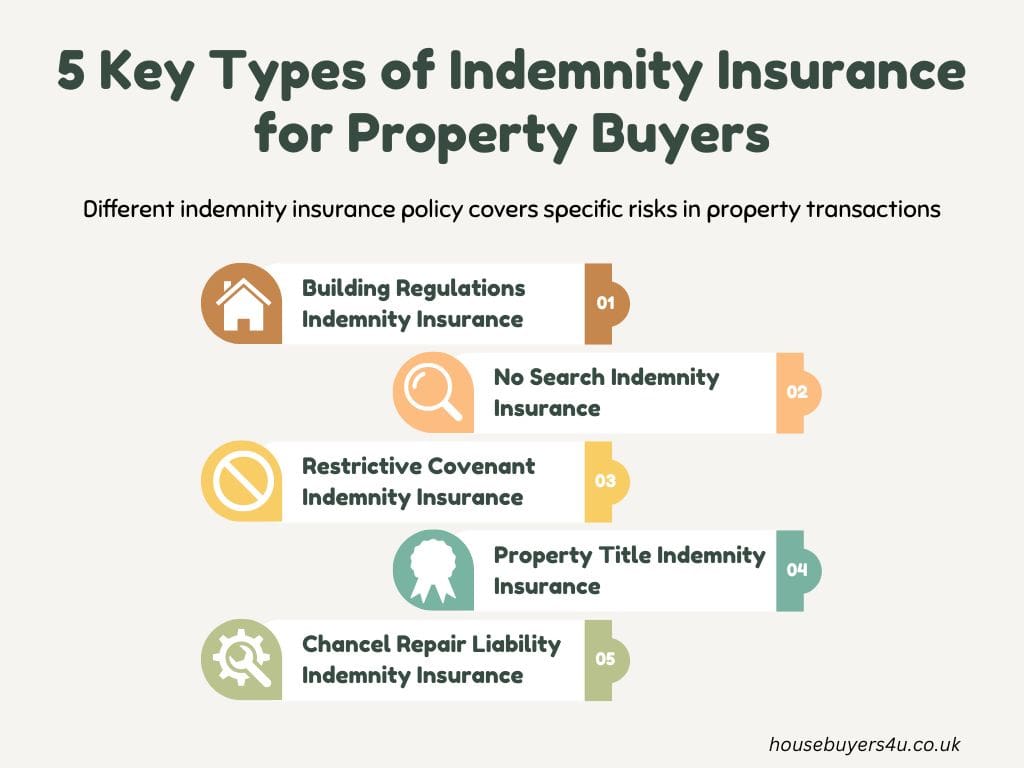

What Does Indemnity Insurance Cover

Different indemnity insurance policy covers specific risks in property transactions:

-

Building regulations indemnity insurance: If a previous owner modified or extended a property without the necessary planning permissions, you might face issues. Seeking retrospective planning permission can be a risky and expensive process. Building regulations indemnity insurance protects you if the local council demands costly modifications.

-

No search indemnity insurance: Sometimes, standard property searches are not conducted. This insurance protects you from surprises that these searches would have uncovered.

-

Restrictive covenant indemnity insurance: If your property comes with restrictive covenants or rules on what you can’t do and you accidentally breach them, this insurance helps manage any claims against you and covers legal fees or fines.

-

Property title indemnity insurance: Issues with your property's title? This insurance helps you with discrepancies or claims against your ownership.

-

Chancel Repair Liability Indemnity Insurance: This is a lesser-known but prudent consideration for properties located near churches with historical entitlements. This insurance protects you against the financial impact of these ancient ecclesiastical charges.

Key Considerations on Indemnity Insurance

For most sellers, the cost of indemnity insurance is a one-off payment that’s minor compared to the risk of a sale falling through or paying for expensive legal work, and having a policy in place can also make your property more attractive to buyers in the future by showing any potential legal issues have already been addressed.

Expert comment from our Property Expert, Paul Gibbens:

"Most sellers only discover they need indemnity insurance when a buyer’s solicitor flags something up at the last minute. It’s a quick fix that saves a lot of stress, and it’s often the difference between keeping your sale moving or starting again from scratch.

For most sellers, the cost of indemnity insurance is a one-off payment that’s minor compared to the risk of a sale falling through or paying for expensive legal work, and having a policy in place can also make your property more attractive to buyers in the future by showing any potential legal issues have already been addressed."

How Does Indemnity Insurance Affect the Sale Process?

If a legal issue is flagged during the conveyancing process, your solicitor will advise if indemnity insurance is needed and arrange the policy for you. The seller usually covers the cost, but it’s often negotiable and sometimes split between the seller and the buyer. Most policies can be set up within a few days, so they rarely delay completion. Acting quickly with indemnity insurance can help avoid stalled sales, collapsed chains, and last-minute stress for everyone involved.

How Much Does Indemnity Insurance Cost?

Indemnity insurance is often viewed as a prudent way to mitigate potential legal risks associated with property transactions.

It’s a one-time investment that covers you for as long as you own the property, and the cost can really vary depending on several factors.

| Scenario | Typical Cost | Notes |

|---|---|---|

| Standard legal issues (e.g. missing FENSA, unapproved work) | £100–£500 | The most common range for house sales |

| High-value properties | £500–£2,000+ | Cost increases with property value |

| Complex legal defects or multiple issues | £1,000+ | Rare usually only for major or multiple legal problems |

| Negotiated/shared cost | Varies | Sometimes buyers/sellers split the cost, ask your solicitor |

Frequently Asked Questions on Indemnity Insurance