Selling a House with a Mortgage UK: What You Need to Know

Yes, you can. Selling a house with a mortgage is standard practice in the UK. When you sell, your solicitor uses the sale proceeds to pay off the remaining mortgage balance, so you don’t need to worry about clearing the loan yourself in advance.

Key Takeaways:

- Selling with a mortgage is routine; your balance is paid off from the sale.

- You can pay off your mortgage or transfer (“port”) it to your next home.

- Early planning helps you avoid delays and negative equity risks.

How Does Selling a House with a Mortgage Work?

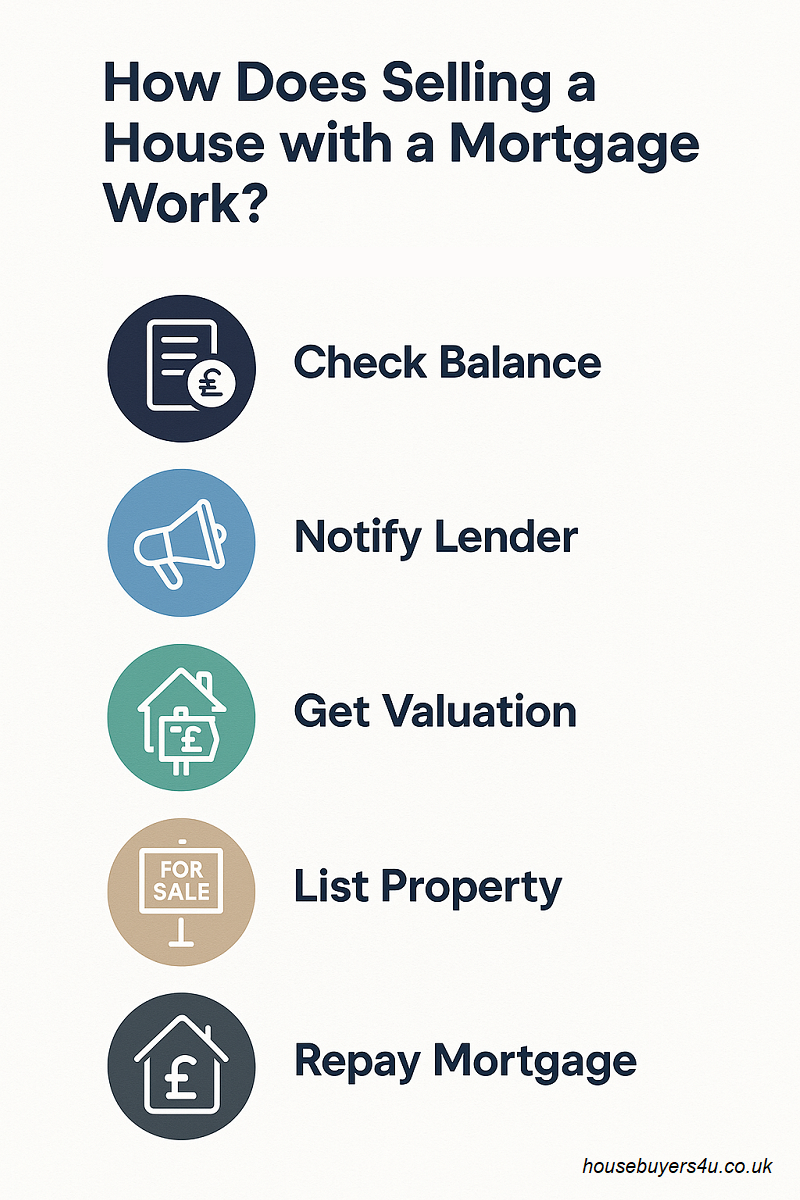

Here’s how the process typically goes, step by step:

-

-

Check your outstanding mortgage balance. Ask your lender for a redemption statement so you know exactly what’s left to pay.

-

Inform your mortgage lender. Let them know you’re planning to sell, and they’ll explain any conditions, fees, or options.

-

Get a property valuation. Arrange for an estate agent or surveyor to conduct a valuation to estimate your selling price and ensure it covers your mortgage.

-

Put the property up for sale. List your home and proceed as normal, just remember you’re still responsible for mortgage payments until completion.

-

Solicitor repays mortgage from sale proceeds. On completion, your solicitor uses the sale funds to clear your mortgage balance before releasing any leftover money to you.

-

What Happens to Your Mortgage When You Sell?

When you sell your house with a mortgage, your solicitor handles the financial side by using the proceeds from the sale to pay off your remaining mortgage balance with the lender first. If there’s any money left over after clearing the mortgage and covering legal or estate agent fees, you receive the remainder. You won’t need to pay off the mortgage yourself in advance; just keep making payments until the sale completes, and your solicitor takes care of the rest.

Government figures show that roughly 35% of UK mortgage lending now goes to home movers, highlighting how common it is for sellers to repay mortgages from sale proceeds.

Expert insight from Paul Gibbens, Housebuyers4u:

"When you sell a house with a mortgage, most people don’t realise just how much smoother things run when your solicitor and lender are kept in the loop right from the start. I always advise our clients to get their redemption statement early and let us handle the coordination. This avoids stress, speeds up the process, and means you’re never left wondering what happens to your mortgage money on completion."

Is Porting Your Mortgage the Right Move? (Pros & Cons)

If you’re thinking about moving but want to keep your current mortgage deal, porting could be an option. Here’s what to weigh up:

Pros of Porting a Mortgage

-

Lets you keep your current interest rate, which is ideal if rates have risen since you fixed.

-

Helps you avoid early repayment charges on your existing mortgage.

-

Makes moving home simpler, fewer changes, and less paperwork than starting a new mortgage.

Related read: Paperwork needed to sell a house in the UK

-

It can save you money if your existing deal is better than what’s currently available.

Cons of Porting a Mortgage

-

Not all mortgages can be ported; always check with your lender first.

-

Your lender will reassess your finances, so you’ll need to pass new affordability checks.

-

If your new property is more expensive, you might need a top-up loan (which could be at a higher rate).

-

Some lenders charge admin fees or restrict which properties qualify for porting.

Should You Pay Off or Port Your Mortgage?

Whether you should pay off your mortgage or port it depends on your financial situation and the terms of your current deal. If you’re on a great fixed-rate or would face hefty early repayment charges, porting your mortgage to your next property can save you money and hassle. However, if your deal is ending soon or better rates are available, paying off your mortgage and starting fresh could make more sense. Always check the fees and small print, and compare your options carefully.

Real Hb4u Insights: Selling a House with a Mortgage

We've gathered data and compiled a list of key insights for selling with a mortgage.

| Insight | What We See at Hb4u |

|---|---|

| Sellers with unconfirmed mortgage balances | Cause 65% of delayed completions always get your redemption statement early. |

| Porting vs. paying off | Only 1 in 4 sellers choose to port; most pay off the mortgage with sale proceeds. |

| Common cause of late-stage problems | Early repayment charges surprise 30% of sellers ask your lender about fees upfront. |

| Most common questions from sellers | “Will my mortgage be cleared automatically?” and “Can I sell if I’m in a fixed term?” |

| Time from offer to completion (with mortgage) | 85% of our sellers complete within 8–10 weeks when the paperwork is ready upfront. |

Don’t Stress About Your Mortgage - Sell with Housebuyers4u

Selling a house with a mortgage is a normal part of moving, but early planning makes all the difference. Double-check your balance, talk to your lender, and consider your porting options before you. These simple steps help you avoid stress, delays, and unexpected costs.

Selling with a mortgage doesn’t have to be complicated. Get in touch with Housebuyers4u for straightforward, no-pressure advice.

Find out how much we can Offer for your House