Upsizing: Should I Buy a Bigger House?

Updated: January 2026

Upsizing is about more than simply buying a bigger house. It usually involves balancing extra space and comfort against higher monthly costs, long-term financial commitments, and the flexibility your lifestyle needs in the years ahead. The right decision depends on whether the added space will genuinely improve daily life without putting pressure on your finances or limiting future options.

Key Takeaways:

- Upsizing can improve day-to-day life, but costs go beyond the mortgage.

- The right move depends on timeline, income stability, and future plans.

- Most regret comes from underestimating running costs and overbuying space.

What Is Upsizing?

Upsizing means selling your current home and moving to a larger property to gain more space or a layout that better suits your lifestyle or future needs.

Should you Upsize?

You should consider upsizing if your current home no longer works for your daily life and you can afford the higher costs without stretching your finances. It is usually not the right move if your income is uncertain, your budget is already tight, or the extra space is unlikely to be used long term. Check running costs, future plans, and whether the move solves a real problem before committing.

Common Reasons People Consider Upsizing

-

Growing family

-

Home office needs

-

Desire for more amenities

-

Investment potential

-

Lifestyle changes

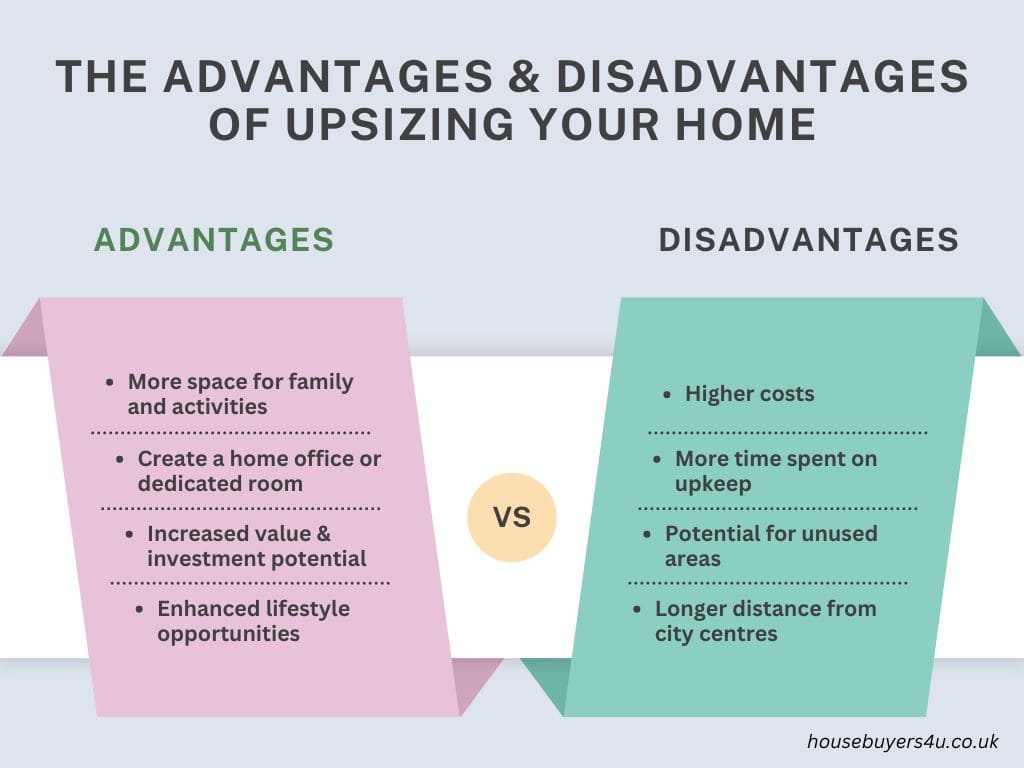

The Advantages and Disadvantages of Upsizing your Home

Advantages

-

More space for family and activities: A larger home means more room for everyone. Whether it’s giving each child their own bedroom, creating a dedicated playroom, or just enjoying more space to relax, a bigger house can make daily life more comfortable.

-

Potential for home office or dedicated rooms: With remote work becoming more common, having a dedicated office space is a big plus. A bigger home might also offer the chance to create other useful spaces like a home gym, guest room, or hobby room.

Before upsizing, take a hard look at your lifestyle and how you use your current property. It’s easy to get excited about extra living space, but if they end up sitting empty, you might regret the move.✕ -

Increased property value and investment potential: Larger homes in desirable areas tend to appreciate more over time, offering strong investment potential. Selecting the right property could result in significant financial gains down the line. In fact, according to Zoopla, the average UK house price is projected to rise by 1.5% before the end of 2024.

Related Read: How much is my house worth in 2026?

-

Enhanced lifestyle opportunities: A bigger house often comes with perks like a larger garden, perfect for outdoor activities or gardening. Plus, it might mean better access to amenities, schools, or a more desirable neighbourhood.

Disadvantages

-

Higher costs: Your budget should be able to handle the higher mortgage, increased utility costs, and maintenance expenses without causing stress.

-

More time spent on upkeep: More space often means more time spent on cleaning, repairs, and general maintenance. This can eat into your free time, leaving you with less time to enjoy your new space.

-

Potential for unused areas: Extra rooms can be great, but they can also end up being underused.

-

Longer commutes or distance from city centres: Imagine upsizing from a small city flat to a larger house in the suburbs. You gain space and a garden, but now face an hour-long commute. Over time, the strain of the commute and extra costs might make you rethink the move.

The True Cost of Upsizing (Beyond the Mortgage)

Buying a bigger home usually increases your monthly and upfront costs in several areas, not just the mortgage repayment.

-

Mortgage increase: Larger properties typically mean higher monthly repayments, especially if you are borrowing more or moving into a higher interest rate band.

-

Stamp duty: Upsizing often pushes you into a higher stamp duty bracket, which can add a significant one-off cost at completion.

-

Moving costs: Removal services, storage, and overlap costs between homes can quickly add up during the move.

-

Council tax: Bigger homes are more likely to fall into a higher council tax band, increasing annual bills.

-

Utilities and maintenance: Larger properties generally cost more to heat, insure, and maintain, with higher ongoing repair and upkeep expenses.

These costs are often underestimated and are the most common reason homeowners regret upsizing after the move.

What we see in Practice at Housebuyers4u

Based on Housebuyers4u’s internal enquiry and completion data, homeowners who upsize most often underestimate the ongoing costs rather than the purchase price itself.

Most commonly underestimated upsizing costs (Housebuyers4u insights)

| Cost area | How often it surprises sellers | Why it’s missed |

|---|---|---|

| Utilities and heating | Very common | Larger homes cost more to heat year-round, not just in winter |

| Ongoing maintenance | Common | Bigger roofs, gardens, and systems mean higher upkeep |

| Council tax | Common | Band increases are often overlooked until after completion |

| Moving and overlap costs | Moderate | Temporary storage and double bills add up quickly |

| Insurance and repairs | Moderate | Higher rebuild values and more frequent maintenance |

Upsize with Confidence Through Housebuyers4u

Upsizing should feel like an exciting new chapter, not a drawn-out headache. At Housebuyers4u, we specialise in helping homeowners sell their smaller house quickly and stress-free, so you can move on to the bigger home you’ve been dreaming of.

We buy any house in any condition, offer a guaranteed cash sale within 7–14 days, and cover all fees. That means no delays, no chains, and no hidden costs, just a smooth move to your new home.

Frequently Asked Questions