Buying vs Renting

Should you buy or should you rent?

Many people struggle with this question. We have those who simply cannot wait to get on the property ladder and invest everything they have to try and get there. Then there are those who prefer living with less financial burden on rent, but which one is right for you?

Let’s take a look at some of the advantages and disadvantages of both.

Related: Approaching Retirement – Is it Better to Buy or Rent

Buying a house

For many people buying a house and then paying off it’s mortgage is the ultimate financial achievement however, buying a property is not something everyone can handle.

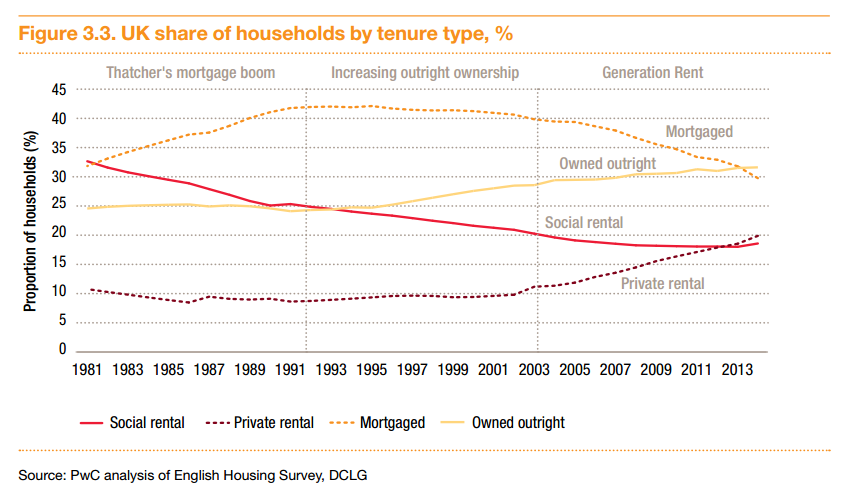

A survey completed by the Building Societies Association states that around half of 25-34 year olds say they may need a mortgage that lasts into retirement.

Furthermore, over a quarter (27%) of people in this age group also think they may struggle getting a mortgage into retirement because their credit history, income level or age will count against them.

This shows that people are not only worried about getting an initial mortgage but also worried that if they had to take out a new one later on in life they may not be able to get it.

It’s not all doom and gloom though. It’s been proven over countless years by many people that it’s possible to get a mortgage and reap the benefits of having your own home. Some of these benefits include:

If you manage to pay off your mortgage entirely the property will eventually become yours. You will never have to worry about paying for somewhere to live.

This cannot be said if you were renting a property as you are living on someone elses property and will always have to pay.

Once your mortgage is approved and you start living in your home you can pretty much do anything you want to it. From painting the walls bright red to adding disco lights to your living room – the choice is yours.

You do not have this option if you were renting a property because you will more than likely have to get permission from the landlord if you wanted to change the look of anything in the home.

Another great benefit of buying a home is you will also be ‘buying’ into the existing community around your home. You now have the opportunity to get to know new people as well as getting involved in things like local charities and sports groups.

Although some long term renters will also benefit from this, generally renters will always be on the move. In addition, sometimes renters cannot control whether they stay in a property. If a landlord wants them out, they will more than likely have to leave.

When you pay off your mortgage you will own the property outright and have a big asset to your name. If you ever needed extra money or wanted to invest in something else you can always use this.

Renters will never have this option. Rent money is effectively dead money – they will never see it again.

Related: The pros and cons of purchasing new build homes

Renting

Research carried out by PriceWaterCooper predicts that London will become a city of renters, with just 40pc owning their own home in 2025.

Not to say this will be the same for the rest of the country but is renting the way forward in Britain? Let’s look at some of the benefits of renting.

You will probably have to pay some kind of deposit when you start renting a home but it does not come close to the amount that you will have to put down if you were purchasing a house.

People who are wanting their own home have no choice, they will have to put down an absolute minimum of 5% market value of the home if they wanted to get a mortgage for it. Even if the property is only valued at £100,000, they will need to save £5000.

While renting you get the added bonus of not being bound to one place and being able to move around to different cities and places with relative ease.

Homeowners do not have this option, they pretty much have to stay the course of the mortgage or risk losing out.

Renters do not have to worry about fluctuating interest rates or the housing market. They do not own the home so it makes very little difference to them if the price of it goes up or down.

People who own homes on the other-hand will always have to worry about this. A change in interest rate could mean they have to start paying more on their mortgage and a change in property prices could put them in negative equity.

All in all, both renting and buying have pro’s and con’s and it really comes down to personal preference and what type of lifestyle you want to live when choosing which one is better.

Related: How to Rent a Property the Right way as a Landlord

{kind=link}